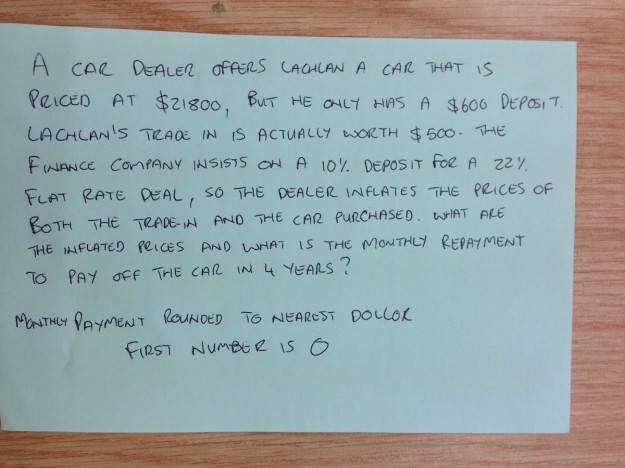

The title caption reads: “A classmate was caught using his phone in maths. The teacher took his phone and set a passcode. He gave him this back with his phone and said good luck unlocking it.”

Hopefully the student was the guy who sits in the back and goofs off because the class is too easy. [via @FryRsquared]

Visualize This: The FlowingData Guide to Design, Visualization, and Statistics (2nd Edition)

Visualize This: The FlowingData Guide to Design, Visualization, and Statistics (2nd Edition)

You can tell the problem was set by a math teacher because of the spelling. Or maybe the teacher was thinking of the dolor the student would feel while solving the problem.

That was the first thing I noticed.

Dolor erit, certe.

High school math, fun times.

So, first to find the inflated value of the car… wait. Doesn’t matter, the loan amount remains fixed because the inflated trade-in of the car doesn’t go on the loan. So the entire math about that is a red herring.

$21800 – $600 cash, – $500 trade in = $20700 loan. Plug that into a loan calculator, and I get $652 and change, making his password 0652.

Plugging it into a loan calculator is cheating.

And what loan calculator did you use? I don’t think that is right. I’m getting $526 a month

Unfortunately his loan calculator was a phone app…

Inflated price because they want 10% down, meaning $2180.

Ah, but you see, today all Math tests and Exams have to be a bit convoluted. Students must be able to read and then pick out te bits of information needed to be able to do the math problem. Also, they would not have access to a loan calculator. And then they have to not only show their work, but also write – in sentences – how they did it.

And the question asks for the inflated price. I don’t see what it has to do with the password, but it says to answer for it.

You need to know the inflated price because the car dealer will take a hit otherwise. So the price of the car must increase along with the trade-in price. That’s an increase of $1200 in both cases.

Nah, the inflated prices don’t affect the starting principal of the loan – they cancel out.

I did do it the hard way before I realised that, by the way, but I shouldn’t have.

Looks like no one is going to get their phone unlocked.

Below is my step-by-step attempt.

Cost of the car: $21,800

Tradein & Cash: $500 + $600 = $1,100

Deposit 22% of car value: $21,800 * .22 = $4,796

Difference to be added to FINANCING: $4,796 – $1,100 = $3,696

Finance Value of the Car/ Inflated Price: $21,800 + $3,969 = $25,496

Rate: 10% in 4 years or 48 months

Equation needed: Monthly payment = P(r/12) / (1 – (1 + r/12)^-m)

P – your finance amount

r – rate in decimal

m – length of loan term in months

25,496(0.1/12) / (1 – (1 + .1/12)^-48)

212.4667 / (1 – 0.671432) = 646.645 or 647

The code is: 0647

Additional items of interest are below:

What’s the “real-price” in 4 years? 646.65 * 48 = $31,039

What’s the interest in 4 years? 31,039 – 25,496 = $5,543

I mis-read the deposit and interest so my post is wrong!

Just get the puk code and set a new pin.

Here’s what I came up with. Could be way off.

Initial purchase price = 21800

Initial trade in value = 600

Initial Cash = 500

Required Down payment = 21800 * 10% = 2180

Amount to inflate = 2180(required down payment) – 500 (cash) – 600 (initial trade in value) = 1080

Inflated purchase price = 21800 (initial purchase price) + 1080 (amount to inflate) = 22880

Inflated trade in value = 600 (initial trade in value) + 1080 (amount to inflate) = 1680

Amount financed = 22880 (inflated purchase price) – 1680 (inflated trade in) – 500 (cash) = 20700

Interst amount = 20700 (amount financed) * 22% (flat interest rate) = 4554

Total repayment amount = 20700 (amount financed) + 4554 (interest amount) = 25254

Total monthly payment = 25254 (total repayment amount) / 48 (monthly payments) = 526.125

Rounded monthly payment = 526 (nearest dollar)

unlock code = 0526

Two problems there, Brian. The first is that the inflated deposit has to be 10% of the inflated price, and instead you’ve used 10% of the uninflated price. Second, you’ve left out interest payments (22% p/a).

Pat – I think that would result in an infinite loop of inflating the price to get to the 10% down payment. Granted, it’s been a long day, and I reserve the right to be wrong. haha.

Great puzzle though.

Nah – the price increases faster than the deposit – from memory, I think they work out when the price is $23k and the deposit is $2300 (but don’t quote me on that).

I think you solved it. But it’s a trick question.

Fully list the terms and everything becomes clear.

Amount financed =

= inflated price – inflated tradein – cash

= (carprice + x) – (tradein + x) – cash

= carprice + x – tradein – x – cash

the x’s cancel eachother out, the amount financed never changes, the unlock code is indeed 0526

You’re right about the canceling – I didn’t realise that until after I’d done it – but you’ve left out interest payments.

You guys from the US shouldn’t by so much stuff with credits…

Inflate car price to 22000 (nice even number)

10% deposit required: 2200

Inflate trade-in to 1600, plus cash deposit 600 equals 2200

New car price minus deposit equals 19800

19800 times interest rate 22% equals 4356

19800 plus interest owed 4356 equals 24156

24156 divided by 4 years equals 6039

6039 divided by 12 months equals 503.2…

Code is 0503

So you increase the cost of the purchased vehicle $200 but the trade inflates by $1100? Don’t know a car dealer that would do that. If you do, they are about to get a lot of business.

I get same answer as Myrddin.

N is the amount the price of the car and the value of the trade-in is inflated by. What the dealer gives up in the inflated trade-in, he makes back in the inflated price.

$21,800 + N = inflated car price

0.1 * inflated car price = inflated deposit

inflated deposit – $1,100 = N

Therefore,

0.1*(21,800+N)-1100=N which solves as N=1200

Inflated car price = $21,800 + $1,200 = $23,000

Inflated trade-in price = $500 + $1,200 = $1,700

To calculate monthly payments, I assume interest is calculated monthly

$23,000, 48 months, 22%/12 = 1.833%/mo

I get payments of $652.18 per month.

Code is 0652

Slight correction, the amount financed was calculated from $20,700, not $23,000. The answer is unchanged

Marc – so close, but it is in fact 526.125 – $526 a month, and a final payment of $532, I presume.

It’s a flat rate loan, so (20,700×1.22)/48.

Actually, you need to use a loan calculation formula to correctly apply the monthly principal coming off.

X=P*[(r*(1+r)^n)/(1+r)^n-1]

X is monthly payment, P principal, r interest rate (monthly), n term length (months)

Monthly payment comes out to 652.

Also inflated price of car is $23,000:

(21800+x)*.1=600+500+x

What is the core of this?

Payment+Tradein Payment+Tradein + X = (carprice + X)*0,1

Put in the values and solve for X

600+500 + X = (21,800 + X) * 0,1

X = 2,180 +0,1 X – ,1100

0,9 X = 1,080

X = 1,200

-> Inflated Tradein = 1,100 + 1,200 = 2,300

-> Inflated Carprice = 21,800 + 1,200 = 23,000 (-> Inflated Tradein is indeed 10% of this)

Amount to finance:

Inflated Car price – Inflated Trade in + Flate rate

= 23,000 – 2,300 + (23,000-2,300)*0,22

= 20,700 + 4,554

= $25,254 Total Loan value

So payment for 48 months is

25,524 / 48 = 526,125

—–> PIN is 0526

Like previous comments said already